<p style=" margin: 12px auto 6px auto; font-family: Helvetica,Arial,Sans-serif; font-style: normal; font-variant: normal; font-weight: normal; font-size: 14px; line-height: normal; font-size-adjust: none; font-stretch: normal; -x-system-font: none; display: block;"> Biglari Holdings 2013 Letter To Shareholders

About the author:Canadian Valuehttp://valueinvestorcanada.blogspot.com/

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

BH STOCK PRICE CHART

421.99 (1y: +4%) $(function(){var seriesOptions=[],yAxisOptions=[],name='BH',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1371790800000,404.21],[1372050000000,400.24],[1372136400000,408.63],[1372222800000,408.3],[1372309200000,409.55],[1372395600000,410.4],[1372654800000,412.85],[1372741200000,414.99],[1372827600000,412.42],[1373000400000,415.38],[1373259600000,415.82],[1373346000000,415.63],[1373432400000,414.81],[1373518800000,418.35],[1373605200000,418.7],[1373864400000,423.71],[1373950800000,422.5],[1374037200000,425.16],[1374123600000,433.98],[1374210000000,430.8],[1374469200000,428.72],[1374555600000,425.13],[1374642000000,420.75],[1374728400000,419.33],[1374814800000,419.13],[1375074000000,416.4],[1375160400000,416],[1375246800000,416.56],[1375333200000,421.98],[1375419600000,432.36],[1375678800000,433.97],[1375765200000,428.47],[1375851600000,431.85],[1375938000000,438.7],[1376024400000,441],[1376283600000,438.67],[1376370000000,439.1],[1376456400000,444.77],[1376542800000,442.79],[1376629200000,442.12],[1376888400000,444.5],[1376974800000,449.7],[1377061200000,456.49],[1377147600000,465.99],[1377234000000,431.71],[1377493200000,429.71],[1377579600000,408.6],[1377666000000,413],[1377752400000,418.36],[1377838800000,417.45],[1378184400000,420.31],[1378270800000,420.29],[1378357200000,417.6],[1378443600000,418.13],[1378702800000,418.53],[1378789200000,419.04],[1378875600000,414.05],[1378962000000,414],[1379048400000,417.96],[1379307600000,418.14],[1379394000000,424.49],[1379480400000,425.01],[1379566800000,427.25],[1379653200000,422.51],[1379912400000,422.41],[1379998800000,422.44],[1380085200000,415.12],[1380171600000,419.19],[1380258000000,413.93],[1380517200000,412.67],[1380603600000,414.97],[1380690000000,415.22],[1380776400000,412.05],[1380862800000,413.99],[1381122000000,413.12],[1381208400000,410.62],[1381294800000,410.93],[1381381200000,413.03],[1381467600000,414.26],[1381726800000,415.33],[1381813200000,411.33],[1381899600000,413.05],[1381986000000,414.4],[1382072400000,416.39],[1! 382331600000,416.7],[1382418000000,415.9],[1382504400000,415.64],[1382590800000,419.86],[1382677200000,421.08],[1382936400000,425.57],[1383022800000,431.69],[1383109200000,430.03],[1383195600000,436.02],[1383282000000,437.37],[1383544800000,445.71],[1383631200000,453.21],[1383717600000,454.08],[1383804000000,456.95],[1383890400000,456.46],[1384149600000,455.71],[1384236000000,455.04],[1384322400000,456.74],[1384408800000,456.51],[1384495200000,461.72],[1384754400000,460.25],[1384840800000,460.61],[1384927200000,462.89],[1385013600000,474.58],[1385100000000,478.01],[1385359200000,480.34],[1385445600000,480.79],[1385532000000,483.9],[1385704800000,485.06],[1385964000000,474.87],[1386050400000,481.59],[1386136800000,480.44],[1386223200000,480.59],[1386309600000,490.17],[1386568800000,495.72],[1386655200000,485.34],[1386741600000,479.24],[1386828000000,477.09],[1386914400000,475.31],[1387173600000,483.55],[1387260000000,480.36],[1387346400000,482.68],[1387432800000,488.25],[1387519200000,498.5],[1387778400000,511.06],[1387864800000,519.21],[1388037600000,519.27],[1388124000000,518],[1388383200000,509.95],[1388469600000,506.64],[1388642400000,500.68],[1388728800000,502.17],[1388988000000,485.82],[1389074400000,484.87],[1389160800000,478.7],[1389247200000,476.09],[1389333600000,479.56],[1389592800000,483.21],[1389679200000,491.97],[1389765600000,487.8],[1389852000000,490.02],[1389938400000,486.38],[1390284000000,485.33],[1390370400000,484.51],[1390456800000,474.08],[1390543200000,466.06],[1390802400000,457.35],[1390888800000,445],[1390975200000,441.72],[1391061600000,444.74],[1391148000000,436.96],[1391407200000,425.68],[1391493600000,420.49],[1391580000000,413.62],[1391666400000,419.15],[1391752800000,421.31],[1392012000000,418.04],[1392098400000,429.03],[1392184800000,430.76],[1392271200000,430.28],[1392357600000,430.83],[1392703200000,427.29],[1392789600000,423.01],[1392876000000,429.49],[1392962400000,436.11],[1393221600000,439.77],[1393308000000,440.14],[1393394400000,446.25],[1393480800000,446.04],[1393! 567200000! ,448.99],[1393826400000,445.6],[1

"This is a smart move for them," said Money Morning Defense & Tech Specialist Michael Robinson. "The emerging markets, particularly China, they like a larger screen. Forty percent of the smartphones sold in China recently were five inches or larger. So this larger iPhone really helps segment them, and it comes after the China Mobile (NYSE ADR: CHL) deal. I think this is going to be very successful."

"This is a smart move for them," said Money Morning Defense & Tech Specialist Michael Robinson. "The emerging markets, particularly China, they like a larger screen. Forty percent of the smartphones sold in China recently were five inches or larger. So this larger iPhone really helps segment them, and it comes after the China Mobile (NYSE ADR: CHL) deal. I think this is going to be very successful." Sarah Bentham/AP WASHINGTON -- U.S. consumer spending rose less than expected in May, likely held back by weak health care spending, which could prompt economists to temper their second-quarter growth estimates. The Commerce Department said Thursday consumer spending increased 0.2 percent after being flat in April. Spending, which accounts for more than two-thirds of U.S. economic activity, had been forecast rising 0.4 percent. When adjusted for inflation, consumer spending fell for a second straight month, suggesting spending this quarter could struggle to regain momentum after growing at its slowest pace in nearly five years in the first quarter. Spending in May was probably constrained by weak health care spending as outlays on services barely rose for a second month. Spending on automobiles surged, accounting for more than half of the rise in durable goods outlays. U.S. Treasury debt prices rose on the data while the dollar trimmed gains. Reports on employment to manufacturing and the services industries suggest the economy has rebounded after sinking in the January-March period, but the spending data indicated that growth would probably fall short of expectations. "The consumer spending number is not enough of an acceleration to give confidence to large second-quarter GDP rebound numbers," said Alan Ruskin, global head of G10 foreign exchange strategy at Deutsche Bank (DB) in New York. Second-quarter growth estimates have ranged as high as a 4 percent annual pace. The economy contracted at a 2.9 percent pace in the first quarter, the worst performance in five years. In a separate report, the Labor Department said new applications for state unemployment benefits slipped 2,000 to a seasonally adjusted 312,000 for the week ended June 21. The declining claims suggest a recent streak of payroll job gains above 200,000, is likely to be sustained, lending the economy enough momentum for inflation to start perking up. Inflation Ticking Up A price index for consumer spending increased 0.2 percent in May, rising by the same margin for a third consecutive month. In the 12 months through May, the personal consumption expenditures price index was up 1.8 percent, the largest gain since October 2012. It had advanced 1.6 percent April and should comfort Federal Reserve officials concerned about price pressures being too low. Excluding food and energy, prices also posted a 0.2 percent gain. That followed a similar increase in April. The so-called core PCE price index increased 1.5 percent from a year ago. That was the biggest increase since February last year and followed a 1.4 percent rise in April. Both inflation measures still remain below the Fed's 2 percent inflation target. Inflation, which has been depressed by weak medical care costs and sluggish wage growth, is being watched for clues on the timing of the central bank's first interest rate hike. The Fed, which is scaling back the amount of money it is pumping into the economy through monthly bond purchases, has kept its benchmark lending rate near zero since December 2008.

Sarah Bentham/AP WASHINGTON -- U.S. consumer spending rose less than expected in May, likely held back by weak health care spending, which could prompt economists to temper their second-quarter growth estimates. The Commerce Department said Thursday consumer spending increased 0.2 percent after being flat in April. Spending, which accounts for more than two-thirds of U.S. economic activity, had been forecast rising 0.4 percent. When adjusted for inflation, consumer spending fell for a second straight month, suggesting spending this quarter could struggle to regain momentum after growing at its slowest pace in nearly five years in the first quarter. Spending in May was probably constrained by weak health care spending as outlays on services barely rose for a second month. Spending on automobiles surged, accounting for more than half of the rise in durable goods outlays. U.S. Treasury debt prices rose on the data while the dollar trimmed gains. Reports on employment to manufacturing and the services industries suggest the economy has rebounded after sinking in the January-March period, but the spending data indicated that growth would probably fall short of expectations. "The consumer spending number is not enough of an acceleration to give confidence to large second-quarter GDP rebound numbers," said Alan Ruskin, global head of G10 foreign exchange strategy at Deutsche Bank (DB) in New York. Second-quarter growth estimates have ranged as high as a 4 percent annual pace. The economy contracted at a 2.9 percent pace in the first quarter, the worst performance in five years. In a separate report, the Labor Department said new applications for state unemployment benefits slipped 2,000 to a seasonally adjusted 312,000 for the week ended June 21. The declining claims suggest a recent streak of payroll job gains above 200,000, is likely to be sustained, lending the economy enough momentum for inflation to start perking up. Inflation Ticking Up A price index for consumer spending increased 0.2 percent in May, rising by the same margin for a third consecutive month. In the 12 months through May, the personal consumption expenditures price index was up 1.8 percent, the largest gain since October 2012. It had advanced 1.6 percent April and should comfort Federal Reserve officials concerned about price pressures being too low. Excluding food and energy, prices also posted a 0.2 percent gain. That followed a similar increase in April. The so-called core PCE price index increased 1.5 percent from a year ago. That was the biggest increase since February last year and followed a 1.4 percent rise in April. Both inflation measures still remain below the Fed's 2 percent inflation target. Inflation, which has been depressed by weak medical care costs and sluggish wage growth, is being watched for clues on the timing of the central bank's first interest rate hike. The Fed, which is scaling back the amount of money it is pumping into the economy through monthly bond purchases, has kept its benchmark lending rate near zero since December 2008. As today's Bitcoin startups make the digital currency easier to use, those advantages will become more apparent to the general public, setting off a mass transition away from traditional forms of payment such as credit cards.

As today's Bitcoin startups make the digital currency easier to use, those advantages will become more apparent to the general public, setting off a mass transition away from traditional forms of payment such as credit cards.  The expert featured in this column, Elliott Gue, may or may not own positions in any investment vehicle mentioned here. The views and opinions expressed are his or her own.

The expert featured in this column, Elliott Gue, may or may not own positions in any investment vehicle mentioned here. The views and opinions expressed are his or her own.

Related CNL Market Wrap For June 19: Stocks Little Changed, Gold and Silver Higher Mid-Day Market Update: Kroger Surges On Upbeat Results; Pier 1 Shares Slide

Related CNL Market Wrap For June 19: Stocks Little Changed, Gold and Silver Higher Mid-Day Market Update: Kroger Surges On Upbeat Results; Pier 1 Shares Slide

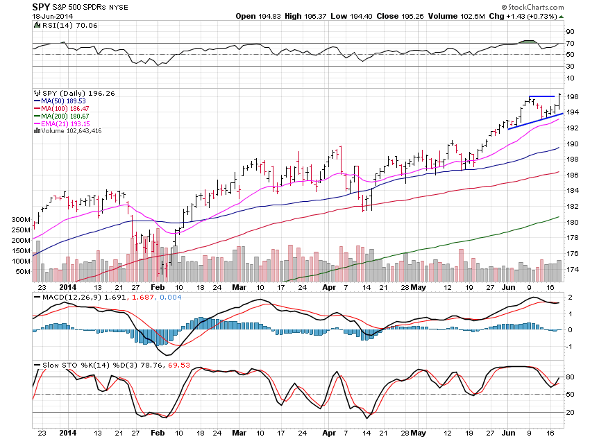

SPY is now breaking out of the wedge pattern and off to the races. Nice volume pushed it to the breakout point which is what I always like to see.

SPY is now breaking out of the wedge pattern and off to the races. Nice volume pushed it to the breakout point which is what I always like to see.

Iraqis turn to Whisper app amidst conflict NEW YORK (CNNMoney) "U.S. Embassy in Baghdad is evacuating..!!!!"

Iraqis turn to Whisper app amidst conflict NEW YORK (CNNMoney) "U.S. Embassy in Baghdad is evacuating..!!!!"  Whisper CEO shares users' darkest secrets

Whisper CEO shares users' darkest secrets